Measure No. 2 - Self-employed who are sickness and pension insured – contribution for self-employed themselves, not their employees

Eligible applicant

It concerns self-employed persons (or “SZČO”) who, at the time of the declaration of an emergency, closed operations or decreased sales.

For the purposes of granting a contribution, self-employed is a natural person who:

- operates a sole trade according to Act no. 455/1991 Coll. on Trade Licensing (Trade Licensing Act), as amended,

- performs activities according to special regulations (eg Act No. 78/1992 Coll. on Tax Advisors and the Slovak Chamber of Tax Advisors, Act No. 323/1992 Coll. on Notaries and Notarial Activities (Notarial Code), Act No. 586 / On Advocacy, Act No. 540/2007 on Auditors, Audit and Audit Supervision), Act no. 185/2015 Coll. copyright law, law no. 103/2014 Coll. on theatrical activity and musical activity, Act no. 40/2015 Coll. On audiovisual, etc.), performs liberal professions that are not regulated by special regulations, and are not a business according to § 2 of the Commercial Code, are a liberal profession, t. j. are activities for the performance of which the law does not require any authorization (eg actor, choreographer, dancer, musician, journalist, sculptor, etc., who are not in an employment relationship or similar employment relationship in the performance of their activities),

- performs agricultural production, including forestry and water management, pursuant to Act No. 105/1990 Coll. on private entrepreneurship.

The condition for the eligibility of the applicant is also that it is a self-employed, who:

- was insured against sickness and pension (compulsory and voluntary) in the period until 30.06.2021 and her insurance lasts even after this day, or her obligation arose from 01.07.2021 and her insurance continues even after this day.

- In the event that SZČO's voluntary sickness and pension insurance starts to pay later, it is entitled to the contribution for the calendar month for which it was voluntarily insured for sickness and pension (at least half of the calendar month) and for the following calendar months during which its insurance lasts continuously.

- draws the so-called paid holidays; it is a SZČO with the beginning of business or implementation / operation of another SZČ in 2020 until the assessment of the establishment of compulsory social insurance as of 01.07.2021, resp. to 01.10.2021 or with the beginning of business or implementation / operation of another SZČ in 2021.SZČO, which started its business in 2020, resp. 2021 and which it was not possible to assess the origin of compulsory social insurance due to the fact that for the calendar year decisive for the origin of this insurance, it did not achieve any income from business or other SZČO.

The contribution cannot be provided to SZČO, which has a canceled or suspended business activity. Applicants for the allowance can only be an entity that was established and started its activities no later than 01.10.2021.

An unauthorized applicant is also a limited liability company.

Contribution conditions:

- In connection with the declaration of an extraordinary situation, state of emergency or state of emergency, his sales decreased

- Self-employed persons was insured against sickness and pension (compulsory or voluntarily) in the period until 30.06.2021 and her insurance lasts even after this day, or this obligation arose from 01.07.2021 and her insurance continues even after this day, or she was voluntarily insured against sickness and pension (at least half of the calendar month) and for the following calendar months, during which the insurance lasts continuously or draws the so-called paid holidays; it is a SZČO with the beginning of business or implementation / operation of another SZČ in 2020 until the assessment of the establishment of compulsory social insurance as of 01.07.2021, resp. to 01.10.2021 or with the beginning of business or implementation / operation of another SZČ in 2021;

- Self-employed persons have no suspended or canceled trade;

- Self-employed was established and started its activities no later than 01.10.2021;

- Decrease in sales due to an emergency

- Fulfillment of tax obligations under Act no. 595/2003 Coll. on Income Tax, as amended,

- Compliance with the obligation to pay advance payments for public health insurance, social insurance and mandatory contributions to old-age pension savings;

- the self-employed person did not violate the prohibition of illegal employment in the two years prior to the submission of the application for a contribution;

- Self-employed persons have no financial liabilities due to the Office;

- is not in bankruptcy, liquidation, receivership, or has no payment schedule specified in a special regulation;

- Self-employed have no unsatisfied claims of their employees resulting from their employment,

- the self-employed person does not have a legally imposed penalty of prohibition to receive subsidies or subsidies or a penalty of prohibition to receive assistance and support provided by European Union funds, if it is a legal person,

- the applicant is not entitled to recovery under a previous Commission decision declaring the aid illegal and incompatible with the internal market.

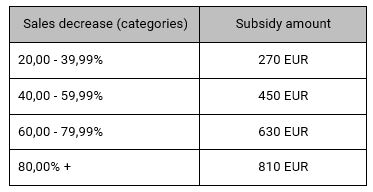

Eligible expenses for the period February 2022

The contribution to compensate for the loss of income from gainful activity for SZČO following the decrease in sales is considered to be eligible expenditure, as follows, at most in the amount of:

If the applicant also has a concluded employment relationship, the amount of net income from this employment relationship for the calendar month for which the contribution is claimed shall be deducted from the amount of the contribution corresponding to the relevant decrease in sales.