Million findings of tax audits focused on transfer pricing

Transfer pricing is gaining popularity not only in the circles of multimillionaires, but also in the circles of smaller companies, sole traders and tax administrations in Slovakia and the world. In additions to the publication of new Guideline of the Ministry of Finance (MF SR) in recent years we saw increasing efficiency of the tax administrator in this area. Given the growing importance of this issue, we will inform you below about basic obligations and new trends in tax audits focused on the area of transfer pricing.

Transfer pricing in short

Transfer pricing is a set of rules that are used to verify the pricing of transactions between dependents. The aim of transfer pricing is to set prices that would be agreed in comparable transactions between independent entities. The introduction of such rules is an effort to combat tax evasion between so-called related persons.

Who is dependent, respectively a related person is defined by the Income Tax Act, which defines these persons as close persons, economically, personally or otherwise related persons, as well as persons or entities that are part of the consolidated group. Assuming your company has such a related person, it is required by law to demonstrate the pricing method in the audited transactions by drawing up transfer pricing documentation.

The content of the documentation is regulated by the Ministry of Finance Guideline no. MF/019153/2018-724 on the determination of the content of the dossier, which was published in December 2018. The taxpayer should proceed in processing the dossier according to the above-mentioned Guideline for the taxation period starting after 31 December 2017. MF/014283/2016-724, which has been in place since 2015. The adoption of this new Guideline strengthened the requirements to document related party transactions and expanded the scope of information required for individual transactions.

It is also important to note that the above rules do not only apply to transactions of foreign dependents, which can be checked retrospectively for up to 10 years, but since 2015 the rules also apply to transactions between domestic dependents that are subject to retrospective check 5 year.

15 day period

The correctness of the method used to determine prices in the audited transactions is generally verified by the tax administrator or the finance directorate in a tax audit. The tax administrator or the Financial Directorate relies transfer pricing documentation for the tax audit. Directorate relies on the transfer documentation in such cases may also serve as an argument to the taxpayer that the prices used in related party transactions have been determined in accordance with the principle of an independent relationship, which may lead to faster tax review.

It is important to note that the tax administrator or the financial directorate is entitled to invite the taxpayer to submit this documentation and the taxpayer is then obligated to submit it within 15 day of the receipt of the call. Given the shortness of this deadline and the shortness of this deadline and the difficulty of drafting the dossier. We recommend you to prepare the transfer dossier every year.

Trends in tax audits

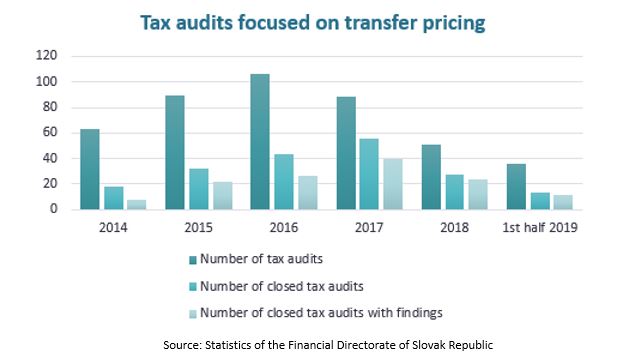

Based on the most up-to-date information, it is evident that tax audits on transfer pricing have been carried out for a long time. If we look at the data of recent years below, we can see that their increasing importance.

So far, most of the tax audits focused on transfer pricing have been performed in 2016, when 106 audits like this was done. Out of the total number of these audits, it was closed in 2017 at the most, the activities of the tax administrator in this area more reflect the figures related to tax audits with the finding and efficiency of its activities.

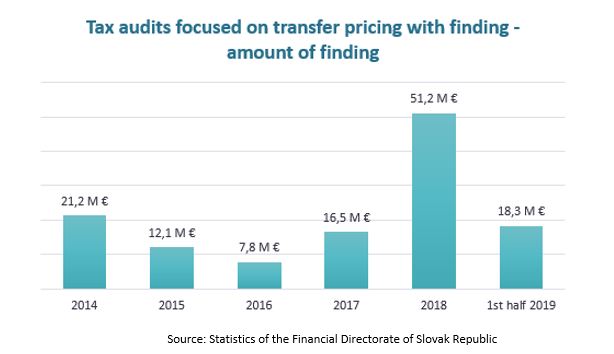

From 2014 until the first half of 2019, at least half of the tax audits with findings were made and completed each year. Already in 2018 and in the first half of 2019, there is a visible increase not only in the number of inspections performed but especially in the efficiency of the tax office to detect shortcomings and inaccuracies in price setting in transactions between dependent persons, so there was a significant increase in the share of completed tax audits with a finding compare to completed tax audits without a finding. On 2018, out of 27 closed tax audits focused on transfer pricing, up to 24 were found and in the first half of 2019 out of 13 were up to 11. As the graph below shows, the findings (even after a slight decline in 2016) amount to millions of euros per year.

Millions of findings and increasing efficiency

The average finding for one tax audit on transfer pricing with a finding for tax audits on other areas of income tax annually. One example is 2018, when the average finding for one tax audit was on transfer pricing with a finding of € 2.131.396, while in other areas it was only € 79.621 on average, which is nearly eighteen times that amount.

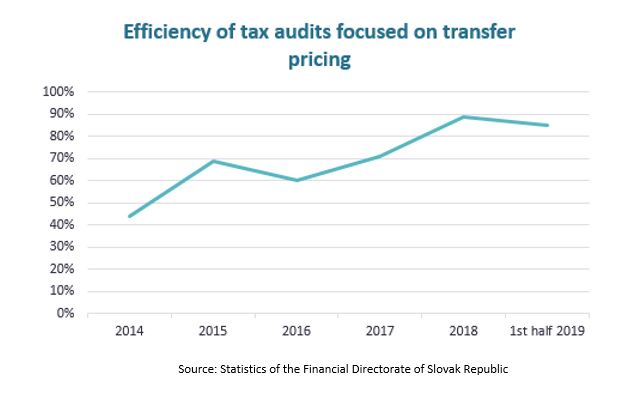

Although the total number of tax audits carried out on transfer pricing has declined over the years, the efficiency of the tax office in these tax audits has gradually improved and is still improving. Compared to 2014, when the level of efficiency of tax administrator did not reach even 50%, in 2018 it was almost unbelievable 89%. The overall development of the tax administrators efficiency in transfer pricing audits is shown in the following chart:

Good advice at the end

Based on practical experience, it is clear that the 15-day period is not sufficient to produce such documentation that would not raise any questions to the tax administrator and terminate the check without additional questions. Therefore, taxpayers are advised to prepare the transfer documentation in time until the tax administrator has started the timekeeper.

Need advice in transfer pricing area?